In some ways, 2020’s “Annual Warehouse and Distribution Center (DC) Equipment Survey” points to a bit of a plateau in spending on equipment and systems. However, that plateau comes after years of healthy investments in distribution centers.

Budgets aren’t skyrocketing, but respondents are well aware of the need to continue to invest to be able to address pressures like tighter cycle times and a scarce labor pool. With many smaller companies in the respondent mix, investment in traditional equipment remains strong, even though there are positives in the survey for newer technologies like robotics.

Norm Saenz, managing director with St. Onge, a supply chain engineering and consulting company that works in partnership with Modern Materials Handling on the study results, believes that the survey shows many positives, but also reflects the reality that many organizations need to layer in some traditional equipment, systems and processes before rushing into technologies like mobile robots, drones or artificial intelligence (AI) applications.

“The future is bright, with the availability of some great technologies for organizations, but the application must fit the particular needs, budget and operational readiness of a business for investments to be successful,” says Saenz.

2020 respondent demographics

Peerless Research Group’s (PRG) e-mail survey questionnaire was sent to readers of Modern Materials Handling and Logistics Management in January of 2020 and early February of 2020, yielding 145 qualified respondents. The respondents were from sites whose primary activity is corporate headquarters (38%), warehouse/distribution (26%), manufacturing (24%), and warehousing supporting manufacturing (10%). The median revenue of responding companies is $58 million, while the average is $268 million, compared with an average of $324 last year, and a median of $84. Qualified respondents—managers and personnel involved in the purchase decision process for materials handling solutions—hold influence over an average of 125,335 square feet of DC space.

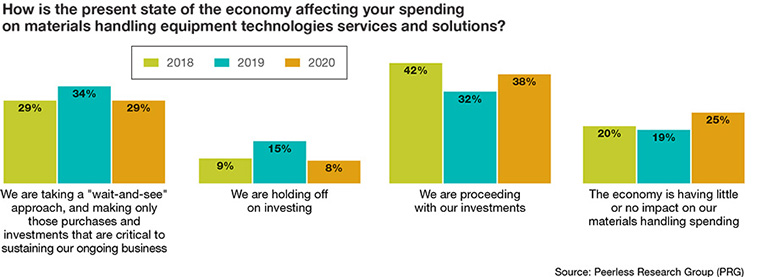

Peerless Research Group’s (PRG) annual survey was conducted in January and early February of 2020, before the supply chain concerns from coronavirus. Among the key spending findings was a drop in those saying they were “holding off” on investing given the state of the economy. This year, only 8% said they were holding off, compared to 15% last year.

Other 2020 highlights include:

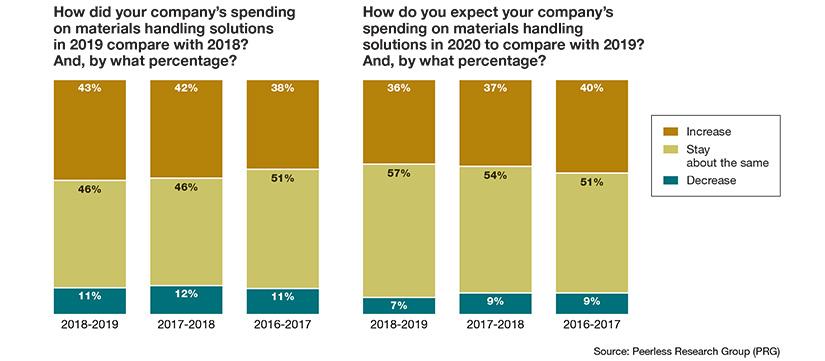

- When asked how 2020 spending would compare to 2019, 36% expect an increase and 57% expect it to stay level. This is a bit more cautious than last year, when 37% expected increased spending, and 54% said it would stay the same.

- When asked about spending expectations over the next two to three years, those foreseeing increased spending dipped, from 53% last year, to 48% this year.

- Spending indications on third-party logistics services stayed steady, even after last year’s increased indications around 3PL services.

- Spending on some traditional equipment categories such as lift trucks and dock equipment stayed steady or grew, while several information systems (IS) categories saw declines. The answers related to robotics were less bullish than last year, but 9% said they currently use robotics, and 19% will consider them during the next 24 months.

- Respondents projected a growing need to automate the measuring of cycle time performance. Respondents also foresee the need for more automation in the way they gauge issues such as on-time shipping and dock-to-stock cycle time.

Overall, the 2020 survey reflects an industry willing to keep up on spending and taking steps to meet ever-increasing fulfillment pressures.

“It’s a fairly cautious outlook, but clearly, people are still going to spend money appropriate to their budgets and operational needs,” says Donald Derewecki, a senior consultant with St. Onge. “Another positive is that the cost of much of this functionality keeps coming down, making solutions more affordable for mid-sized or relatively small companies.”

According to Derewecki, we’re also at a point now when most managers have experience with warehouse systems and software, so there is more fundamental knowledge on how to use these systems. “Clearly, people in industry realize that pressures like faster turnaround time are only going to intensify, and that’s going to require a higher level of control over their operations,” he says.

Spend trends

The 2020 survey showed the overall trend to be healthy, matching the positive spend outlooks of recent years, with some fluctuations. As stated previously, a smaller percentage is holding back on spending due to the state of the economy while 42% are proceeding with investments, up from 32% last year. Those taking a “wait-and-see approach” also declined, from 34% in 2019 to 29% this year.

For those “proceeding with investments,” the survey also asked “on what,” providing broad categories to choose from such as materials handling equipment, IS, conveyors and sortation, robotics, automatic guided vehicles (AGVs), and new this year, “other” as a category. Perhaps partly due to the “other” choice, only 50% indicated plans for IS apps, down from 58% in 2019. This question also found that 22% plan to spend on robotics, down from 40% last year, and nearly as high as the 24% indicating conveyors and sortation.

When asked how spending for the year that just ended (2019) compared to the previous year, 43% said it increased, up 1% from last year, while 46% said it stayed about the same as last year.

Looking to expectations for 2020 spending versus 2019, 36% expect an increase, whereas last year, 37% expected an increase. A majority (57%) expect this year’s spending to stay about the same, a bit higher than last year’s 54%. And for those expecting an increase or decrease, the survey examined by what percentage. This revealed that the median increase was 15%, while the median decrease was 30%.

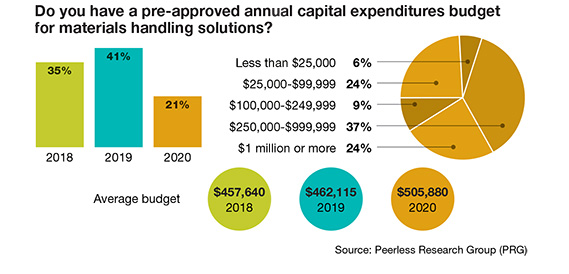

Every year brings a new respondent mix, so dollar findings naturally fluctuate. That said, when asked to pick dollar ranges for total spending over the next 12 months, 5% said their company will spend $2.5 million or more, with a total of 20% spending higher than $500,000. Many respondents also had modest spending projections, with 43% at $99,000 or less.

Average anticipated spending over the next 12 months is $355,175, down from $400,00 in 2019, but higher than 2018’s average. Median anticipated spending for 2020 is $97,905, up slightly from $82,435 last year. For 2020, 36% have an approved budget, and of these, 24% have a budget of $1 million or more. The average budget reached $505,880 this year.

“The respondents are generally optimistic on spending, as seen by the finding that just 8% will hold off on spending,” says Derewecki.

Investment trends

While the last few years have seen gains across various software and technology categories, this year, some of the IS categories declined, with the increases more frequently seen in equipment categories. Of course, in these days of smart, Cloud-connected assets, even traditional equipment can involve technology.

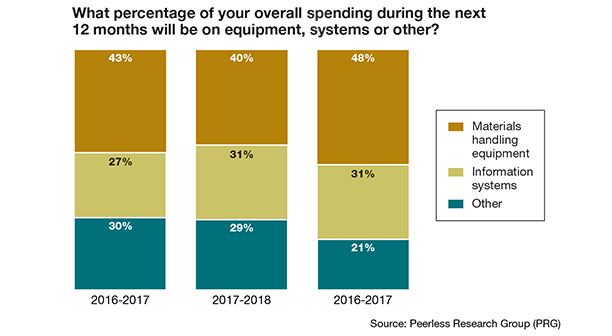

When asked what percentage of overall spending will be on either materials handling equipment, IS, or “other” over the next 12 months, 48% is for equipment, 31% on IS, and 21% on other. Last year, this breakdown was 40% on equipment, 31% on IS, and 29% on other.

Looking at projected 12-month spend for specific categories of equipment/systems, 27% said that they will invest in dock equipment, up from 24% last year. Percentages also bumped up for power transmission including motors, order picking & fulfillment equipment, and automated storage including carousels and vertical lift modules. Spending on lift trucks remained fairly steady, with 46% indicating plans, just 2% lower than last year. Additionally, 16% say they plan to use 3PLs, same as last year.

For projected 12-month spend on IS, several categories were down slightly. One exception is asset management systems, with 26% indicating plans, up from 20% last. Those saying they would spend on transportation management system (TMS) software also stayed level, and 12% have warehouse execution system (WES) plans, down 1% from 2019’s 13%.

For projected 12-month spend on IS, several categories were down slightly. One exception is asset management systems, with 26% indicating plans, up from 20% last. Those saying they would spend on transportation management system (TMS) software also stayed level, and 12% have warehouse execution system (WES) plans, down 1% from 2019’s 13%.

When respondents were asked about broad areas of spending over the next 18 months, most areas were down, with the exception of maintenance services—up 5% to 42%—as well as outsourcing/3PL services, which stayed steady at 13%. This year, only 20% checked enterprise applications as a category for investments over the next 18 months, down from 29% last year.

Saenz notes that for many companies, investment in equipment categories like new lift trucks, dock equipment, or more basic IS areas like bar coding, can be logical improvements if they are coming from older equipment, legacy methods like paper-based pick lists or are expanding.

“There are still many companies that have to make some moves into the more traditional equipment and systems categories—things that have been around for many years—but will help them gain efficiencies and deal with issues like the labor shortage,” says Saenz. “Even the companies forging ahead with the more advanced solutions have to continually evaluate whether they have the right item master data, material flow and processes in place so that when they do layer in the newer technology, it can be effective.”

Robotic & mobile tech

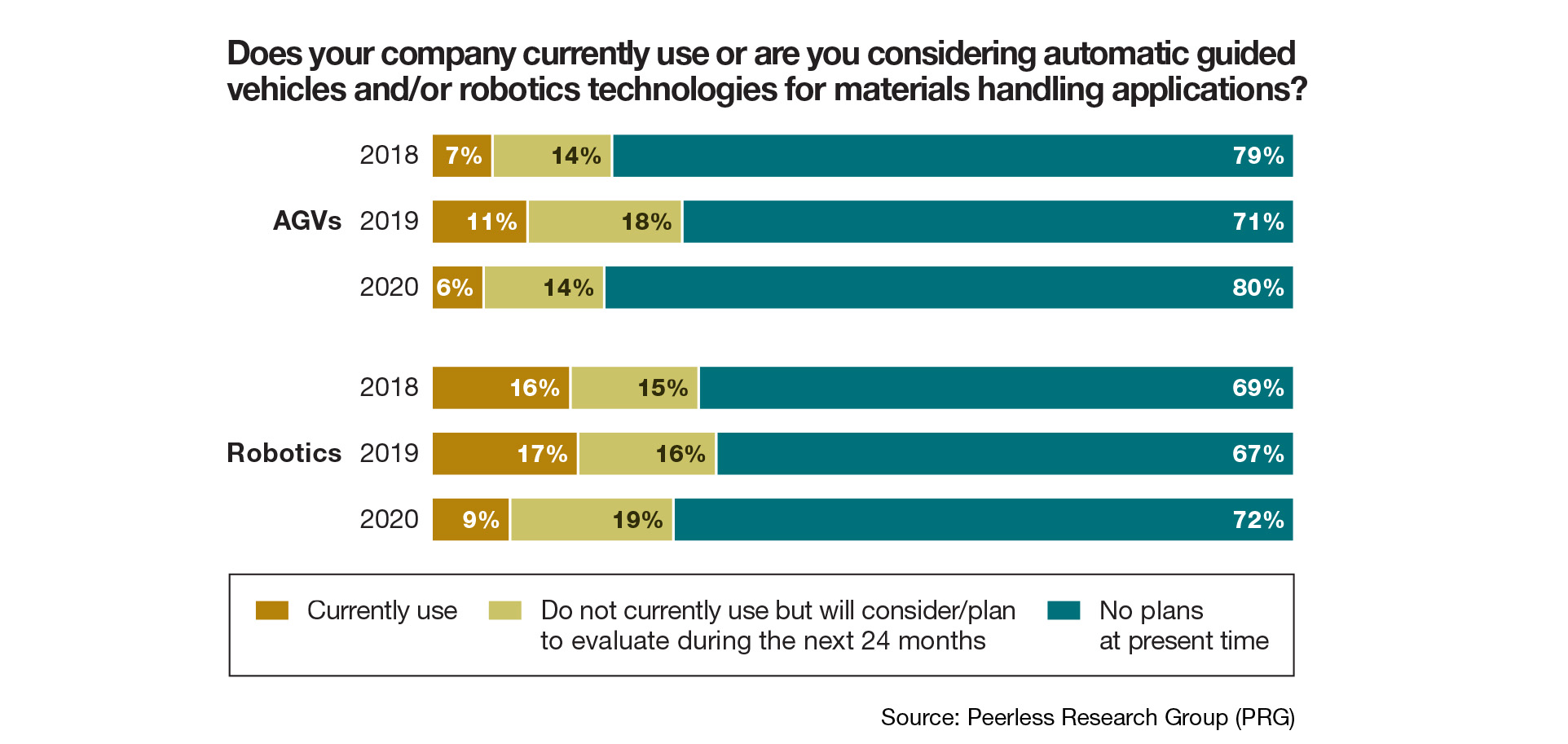

Even though many respondents weren’t from big operations with large budgets, the findings on robots reflect significant activity. For 2020, 9% currently use robotics, down from 17% last year, but 19% are evaluating robotics, up 3% from last year. Additionally, in a separate question that asked those respondents moving ahead with investments in which categories they shall consider, 22% said robotics.

The survey also asked about applications for robotics. Growth applications included packaging (up by 2%), transportation of goods within DCs (up to 18% versus 7% last year), and truck unloading, up by 4%. Palletizing and pick and place remain the two most frequently cited applications for robotics. Mobile autonomous pick to cart held steady at 21%.

The survey also asked about AGV use and applications. AGV use was at 6% this year, with 14% evaluating. This was down compared to 2019, but nearly identical to the AGV use level from 2018. Uses for AGVs on the rise included palletizing (up 4%), depalletizing (up 8%) and packaging, up by 8%.

“The survey has some positive findings on robotics,” Derewecki says. “When you consider the respondent mix, it can be seen as fairly strong uptake level.”

When it comes to mobile technologies, 55% either use or have plans for mobile solutions of some type, up from 52% last year. When asked for current use of and plans for specific types of devices, 53% currently use bar code scanners, and 43% plan to deploy bar code scanners during the next 12 months.

Smart phones and tablets were reported in use by 73%, but only 53% had plans for more during the coming 12 months. One mobile technology forecasted for increased deployment is global positioning system (GPS) technology—in use by 18% currently, but with 28% planning to deploy within 12 months.

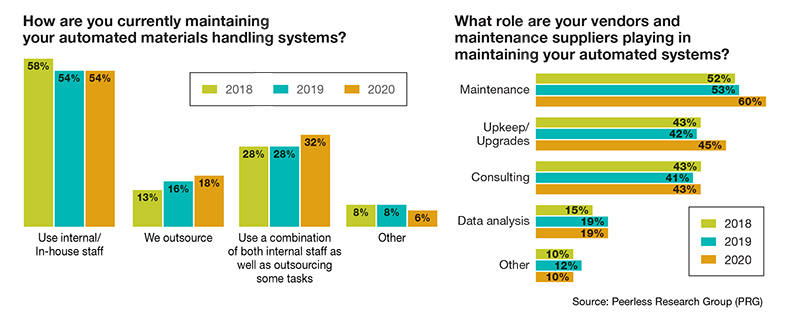

The survey’s findings regarding equipment maintenance showed an increase in outsourcing. This year, 18% said they outsource maintenance of automated systems, up 2% from last year. Additionally, 32% use a combination of internal staff as well as outsourcing for some tasks. Given the increasing level of software and specialized knowledge with today’s automation, this slight uptick is not surprising.

E-commerce trends

When asked for the most common method of fulfilling online orders today, and what the most common method would be in two years, 23% said filling online orders from DCs was currently the most common method, rising to 26% in two years.

When asked for the most common method of fulfilling online orders today, and what the most common method would be in two years, 23% said filling online orders from DCs was currently the most common method, rising to 26% in two years.

Buy online and ship to customer from a store is the most common method for 13% today, rising to 18% in two years. Buy online, ship to customer from vendor is the most common method for 14% today, and rises to 18% in two years. The buy online, pick up in store (BOPIS) method is the most common for just 3% of respondents, with 4% foreseeing BOPIS as the most common in two years.

The survey also asked if e-commerce activity will or is already prompting change in where distribution and manufacturing activities take place. This year, 46% said e-commerce is prompting more distribution functions in manufacturing, up from 42% last year. Meanwhile, 36% said they will perform more manufacturing functions in distribution sites, down from 41% in 2019.

When asked “where does your packaging and fulfillment occur,” the most commonly cited place is a warehouse. This year, 49% said packaging and fulfillment occur at a warehouse, up from 46% last year. Additionally, 20% said packaging and fulfillment take place at a “fulfillment center,” compared to 15% last year, while 17% said that these processes take place in a DC, down from 25% last year. Another 32% said these processes occur in a manufacturing site, down from 37% in 2019. Finally, 9% said these processes occur in retail stores, up from 7% last year.

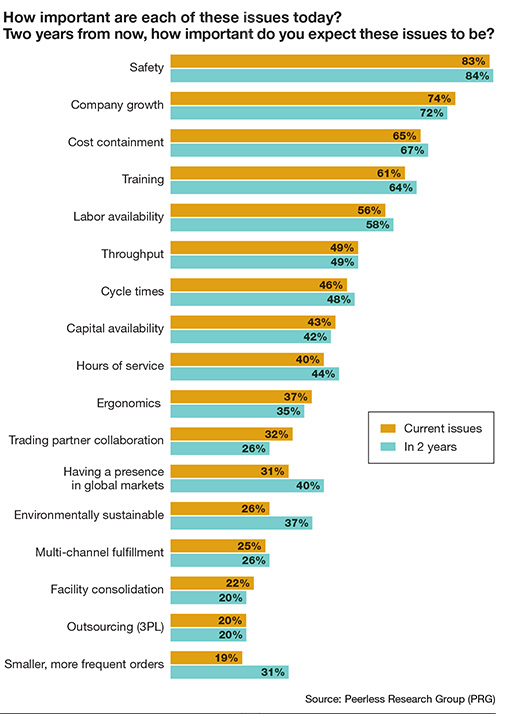

Pressures related to e-commerce such as tighter delivery windows and the labor crunch are reflected in the survey. When asked about the most important issues affecting DCs today and also two years from now, traditional concerns such as safety, growth and cost containment remain the leading areas, but labor availability also is a top concern. Today, 56% said that labor availability is a very important issue, with this rising to 58% in two years. Cycle times also rises by 2% in two years. Smaller, more frequent orders is rated as very important by 19% today, but this rises to 31% in two years.

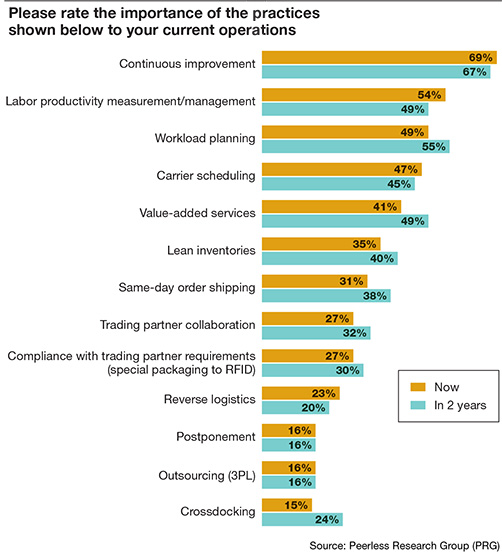

When it comes to DC best practices now versus in two years, the top three practices seen as highly important today are continuous improvement, labor productivity management and workload planning. A bit surprisingly, respondents see labor productivity management as declining in importance two years from now (from 54% today to 49% in two years), though workload planning increases from 49% today to 55% in two years.

Other best practices seen as growing in importance in two years include value-added services, same-day order shipping, and crossdocking. “These results are consistent with what we see among our clients, particularly the growing interest in workload planning and value-added services,” says Derewecki. “Labor availability is a highly important concern for the companies we work with, and it’s surprising to me that it isn’t ranked a bit higher. Of course, if you’re concerned about workload planning, you’re concerned how many people you need to run your operation.”

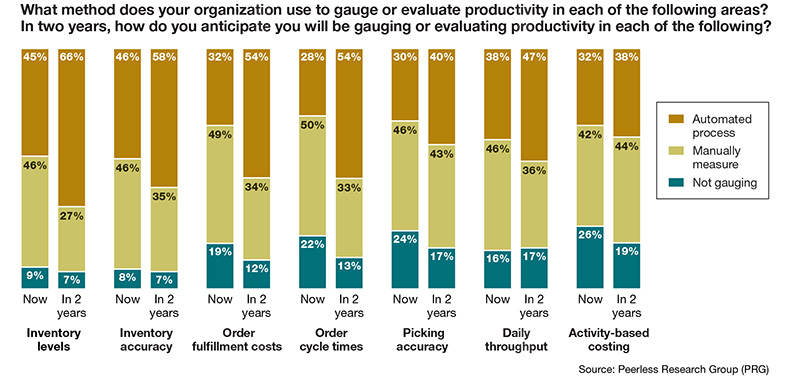

Respondents are also interested in more fully automating the way they gauge the performance of key processes. The survey found only 28% have automated measurement of order cycle time, but 54% expect to have this automated in two years. Another 32% automate the evaluation of order fulfillment costs today, but 54% anticipate automating this in two years.

Similarly, dock-to-stock time is gauged in an automated way by only 18% today, but this increases to 35% in two years. Today, 42% have automated on-time shipping performance visibility. This rises to an anticipated 59% in two years.

Moves to improve

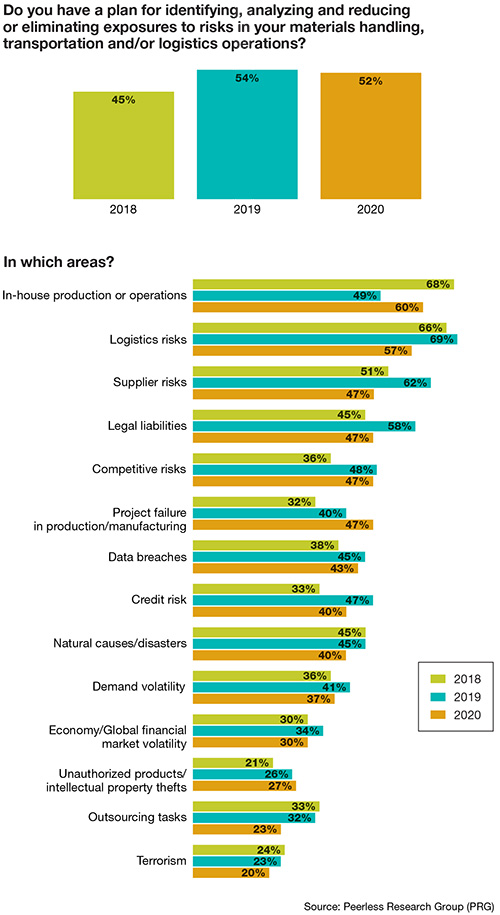

As the survey closed before coronavirus escalated, and North America had a mild winter, supply chain risk concern was muted. This year, 52% said they had a plan for identifying and mitigating risk, down from last year’s 54%, but ahead of the 45% who had such a program in 2018.

The top three risks being planned for were in-house production or operations risks (60%); logistics risks (57%) and supplier risks (47%). Last year, the percentages were higher for logistics risk (69%) and supplier risks (62%). Economic and financial volatility as a risk factor declined from 34% last year to 30% this year, equal to its 2018 level.

The top three risks being planned for were in-house production or operations risks (60%); logistics risks (57%) and supplier risks (47%). Last year, the percentages were higher for logistics risk (69%) and supplier risks (62%). Economic and financial volatility as a risk factor declined from 34% last year to 30% this year, equal to its 2018 level.

With the many operational challenges and logistics risks that organizations face, finding a path to improved performance seems daunting. Some challenges, like the extremely tight labor market or global trade disruption can’t be controlled, only mitigated. The right approach to dealing with these pressures, agree Saenz and Derewecki, is continuous improvement and figuring out which of an operation’s systems and processes need improvement.

As Saenz explains, the right mix of investments varies not only according to budgetary constraints, but how solid an organization is on fundamentals, which can include aspects like having a good material flow, or having accurate item master data in their systems for details like the cubic volume of goods. These foundational elements should come before the shiny, new technologies, Saenz advises.

“Some of the traditional equipment investments can seem boring, but they can be the saving grace for an operation,” adds Saenz. “It’s all about continuous improvement and managers making the right decisions for their business. You have to walk before you can sprint, and find your way to the right mix of investments for your operation.”

About the Author

Follow Robotics 24/7 on Linkedin

About the Author

Follow Robotics 24/7 on Linkedin

About the Author

Follow Robotics 24/7 on Linkedin

Article topics

Email Sign Up