The warehouse automation market has been growing rapidly in the past few years, driven by the need to augment operations with flexible automation to weather the next supply chain shocks and address labor shortages, according to Vecna Robotics. The Waltham, Mass.-based company recently partnered with CITE Research to analyze the current state of the materials handling automation market.

Vecna Robotics and CITE Research surveyed more than 1,000 supply chain professionals industries including automotive, third-party logistics (3PL), consumer goods, manufacturing, e-commerce, and retail. They said their goal was to uncover key trends, challenges, and opportunities in the market.

The robotics vendor and research firm listed the following major trends:

- Warehouses are facing a significant labor shortage: The majority of the market is 10% to 25% understaffed, with material handlers and forklift drivers to move pallets representing the largest labor gaps at 34% and 31%, respectively.

- Automation can help: Most supply chain professionals view automation as a positive for workers, with 70% highlighting improved retention, and over half recognizing it as a means to upskill employees and create job opportunities.

- Autonomous pallet moving has just started to scale: Automation remains largely untapped, with 76% of companies having never deployed an automated guided vehicle (AGV), and 70% never implementing an autonomous mobile robot (AMR). Nevertheless, larger facilities are embracing automation, with 50% of those exceeding 1 million sq. ft. having introduced AMRs. E-commerce leads the adoption rate at 39%, with automotive closely behind at 38%.

- Case picking is everywhere: The majority of respondents (78%) are already using case picking in their operations, with 90% using it in the consumer goods industry, but this task is almost completely performed manually today, said Vecna and CITE.

By 2025, the global warehouse automation market could expand to $69 billion, projected Interact Analysis.

“The following data will help us understand the drivers, barriers and financial considerations of adopting automation,” stated Vecna. “In addition, the data informs how to achieve automation at scale to offset increasing product demand and global supply chain disruptions while keeping existing workers happy.

To deploy or not to deploy, that is the question

As the materials handling space faces a multitude of problems, companies are turning to automation to help, with 85% of respondents planning to deploy some form of automation in the next 12 months, said Vecna Robotics and CITE Research.

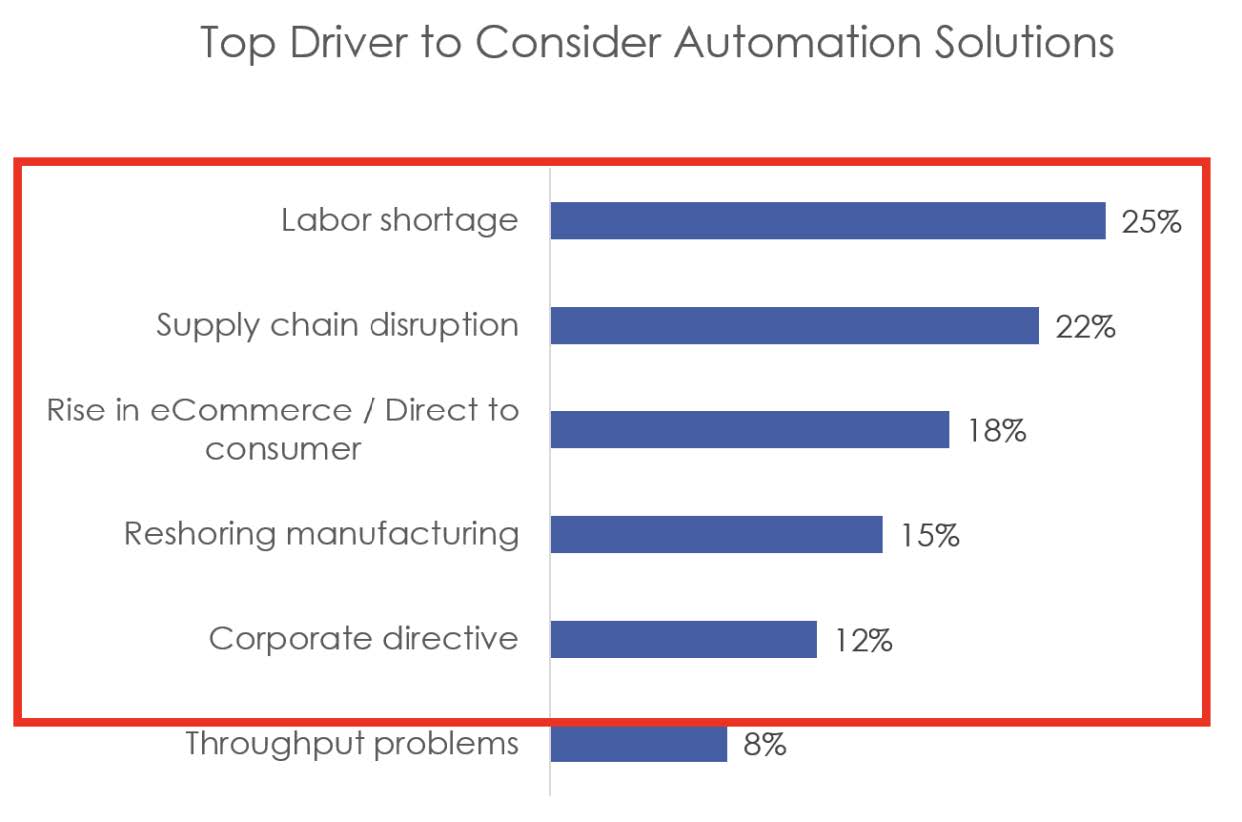

Drivers for automation adoption

Unsurprisingly, the primary drivers for robotics adoption are the labor shortage (25%) and supply chain disruption (22%), said survey respondents.

Smaller facilities are particularly affected by the labor shortage, while larger facilities are more concerned about supply chain disruption. Among industries, retail and e-commerce are most affected by the labor shortage and supply chain disruptions, found the survey.

Barriers to automation

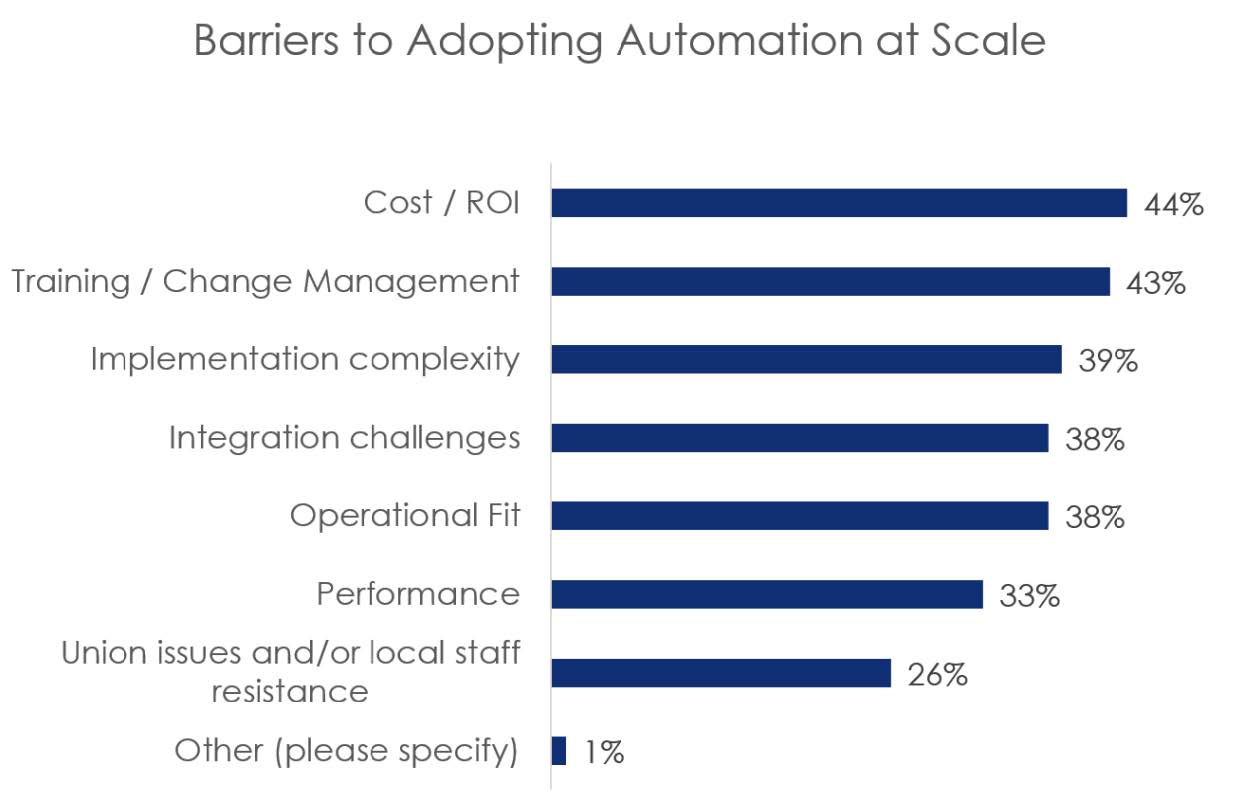

It's no secret that automation is gaining steam, with four in 10 reporting a strong return on investment (ROI) from previous deployments, a number of obstacles remains to adopting automation, noted Vecna Robotics.

In today's volatile economy, cost concerns are at the top of the list of obstacles to implementing automation solutions, with budget (41%) and cost/ROI (40%) being the most significant. Cost and ROI were also the main obstacles to adopting automation efforts previously, with 54% of supply chain professionals stating that it has hampered their implementation plans.

Digging into the data, Vecna and CITE said they discovered that all barriers to adoption show a negative correlation with facility size, except for cost/ROI. Surprisingly, the larger a company's revenue, the more budget and cost and ROI become obstacles to adoption. They said this could reflect the following:

- Long-term strategic vs. short-term ROI: Decision makers at larger firms may be under more pressure to show short-term returns to their business unit in comparison smaller companies that have more runway to consider automation as a strategic long-term investment and competitive differentiator.

- Capex vs. opex models: Dated capital expenditure models are delaying rapid adoption of automation at scale.

- Proven value: New technologies have to do a better job at proving value in environments with more financial discipline and to compete with other types of tech investments. Respondents were not interested in “science projects.”

When it comes to adopting automation at scale, the barriers remain spread. Cost and ROI remained the top barriers (44%) but was followed closely by training/change management (43%). Implementation complexity (39%), integration challenge (38%), and operational fit (38%) also represented significant barriers to adopting automation at scale, said Vecna.

Interestingly, facilities exceeding 1 million sq. ft. behaved differently than the average-sized facility. Their main barriers to adoption were performance, implementation complexity, integration challenges, and training/change management.

“Our analysis also reveals that the 3PL industry is the least affected by these obstacles, while the consumer goods sector is the most impacted,” Vecna said.

What technologies are facilities looking to adopt in 2023?

Automation isn’t the only technology that's top of mind for supply chain professionals, said Vecna Robotics and CITE Research. When asked to prioritize technologies for 2023, respondents shared the following feedback:

- 5G wireless led the way in deployment and is projected to have the most widespread adoption in the near term, with 41% of respondents planning to deploy within the next 12 months. The manufacturing sector is poised to be a major adopter of this technology, with close to 50% looking to deploy within the next 12 months.

- Information technology (IT), such as warehouse management systems (WMS) or enterprise resource planning (ERP), were next on the list with 38% of warehouses planning to deploy in the next 12 months. Automotive (44%) and manufacturing (42%) were set to be the biggest adopters.

- Battery and charging technologies followed closely, with 37% of facilities planning to implement them in 2023. Consumer goods far outpaced other industries in terms of adoption.

- Racking and storage equipment came in fourth, with 35% planning to deploy in the next 12 months. Consumer goods was set to be the largest adopter (41%), and respondents said they expected retail to be the lowest adopter (15%).

- Material handling equipment (MHE) including robotics for pallet-sized loads is still in its early stages, with 31% of facilities surveyed planning to deploy in 2023. There is no real material difference across industries when it came to pallet-sized robot adoption, with automotive set to be the largest adopter (36%), and retail expected to be the lowest adopter (22%).

Investing in automation

While MHE robotics is still in the early stages, it's a promising prospect for the industry, so much so that almost 70% have budget earmarked for new material handling automation within the next year. Vecna Robotics and CITE Research examined financial considerations for the adoption of automation and who is making those decisions.

What are the financial considerations?

When it comes to procuring new technologies and adopting automation in the warehouse, supply chain professionals generally have three options, said the partners:

- Obtaining new technology and automation solutions as a capital expenditure (capex)

- Obtaining them as an operating expense (opex)

- Leasing the technology from a third party (capex or opex depending on the lease)

When the cost of automation often exceeds the signing authority of a warehouse manager, funding will come from a capex budget controlled by upper management. Thus, the proposal may be one of many competing for limited funds allocated across the company.

However, according to respondents, the capex approval process does not appear to be a significant hindrance to adoption, with 89% saying their companies' capex approval process is supportive of automation.

Leasing is another common method to purchase material handling equipment, but the problem is that model is dated when it comes to automation technology. For example, one can lease automated material handling equipment.

However, the equipment itself is typically only a fraction of the overall cost. Critical services like deployment, maintenance, software updates and support services are not typically included in the lease. If not accounted for, they could bust ROI forecast models.

RaaS to the rescue

With robotics-as-a-service (RaaS) models like those offered by Vecna, material handling systems are available as an annual operating expense, enabling companies to update or increase their robot fleets as their needs evolve. RaaS models also tend to include all associated services and support, and are contractually bound to key performance inidicators (KPIs) and uptime service-level agreements (SLAs).

Survey respondents said they expect this flexible and scalable pricing plan become more common, with 84% saying that it would accelerate adoption. When looking at facility size, the report found that the larger the facility or company, the more likely it is to adopt RaaS.

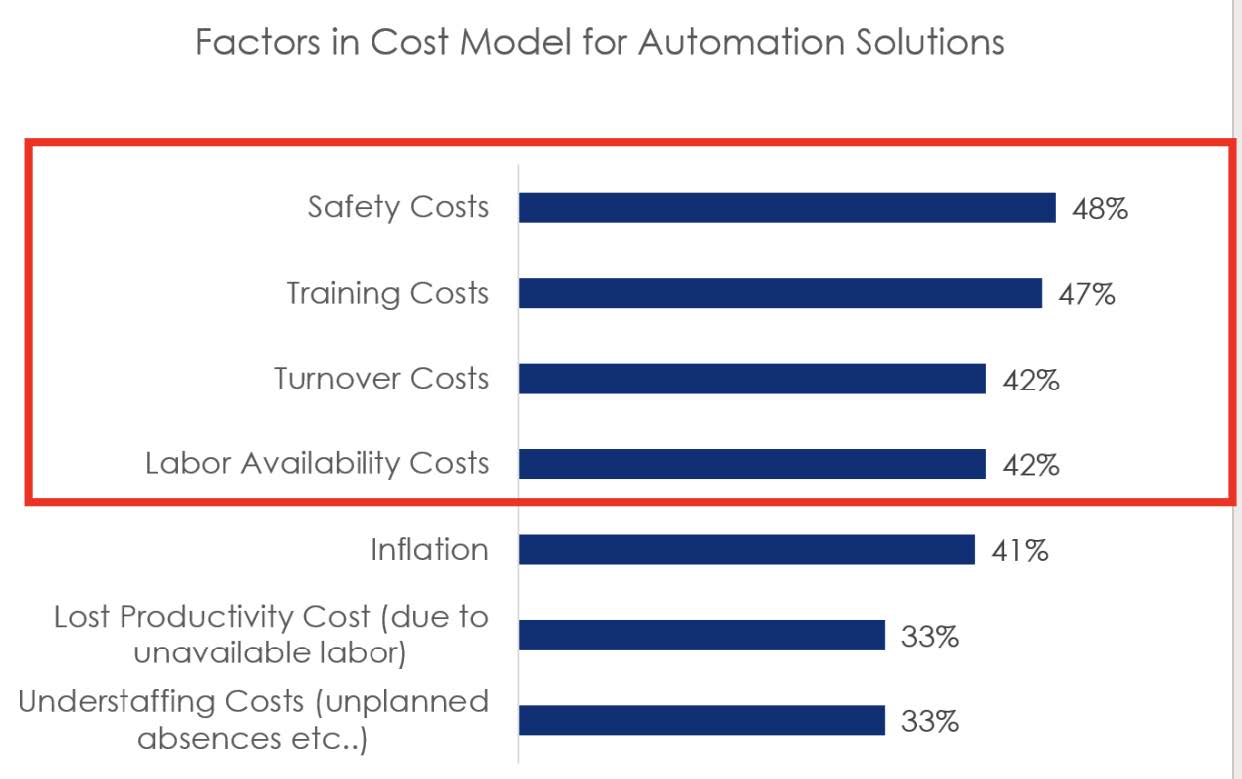

When building a cost model for automation solutions, companies most consider safety costs (48%), training costs (47%), turnover costs (42%), and/or labor availability costs (42%) in addition to wages and benefits.

Breaking this down by facility size and industry, larger facilities are more sensitive to these cost factors. On an industry basis, the consumer goods industry is more sensitive to most cost factors, said Vecna and CITE Research.

Who are the decision-makers?

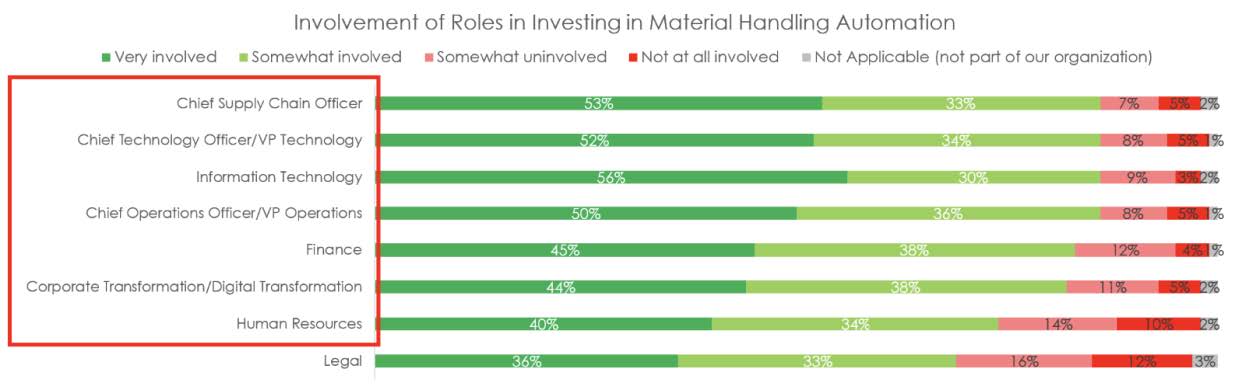

Various parties are involved in material handling automation investments, with the majority of respondents reporting that all roles, from chief supply chain officer to human resources (HR), are at least somewhat involved in investing in automation. However, chief operating officers, chief supply chain officers, chief technology officers, and IT are the most involved parties when it comes to investment.

For any material handling automation projects being considered, the majority of decisions (35%) are made by regional or line executives in charge of multiple facilities, while the next highest was C-level decision makers at 25%.

Vecna and CITE Research said that further analysis revealed that:

- Finance, IT, and HR are more involved when facilities are larger.

- IT is more involved in the decision-making within the consumer goods and manufacturing industries.

- Corporate transformation/digital transformation was very influential when it comes to investing in automation in the consumer goods industry.

- HR gets more involved in the decision-making process when the facility size or company’s revenue is larger.

Getting to scale

So, how does automation become mainstream? Vecna and CITE Research looked at what is affecting automation adoption at scale:

- The economic downturn is not significantly impacting adoption. Seventy-four percent of automation projects have not been affected by fear of economic downtown. In fact, 15% are accelerating adoption. However, 26% of respondents reported that automation projects have been postponed or delayed indefinitely due to economic headwinds.

- Larger companies require a corporate strategic imperative to drive automation projects. Around 50% of companies with $1 billion or more in revenue rely on sucn an imperative to adopt and scale automation.

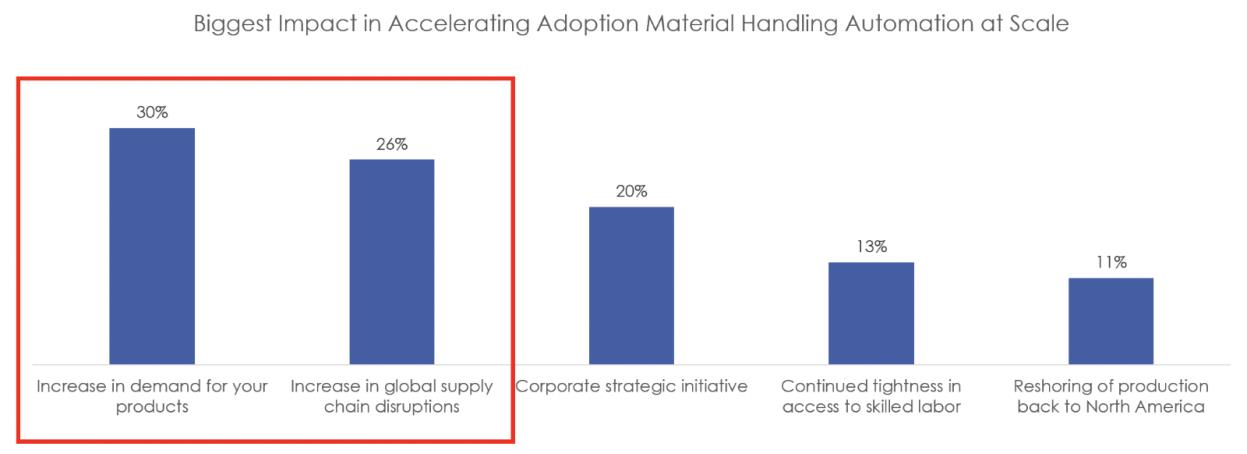

- Increasing product demand and global supply chain disruptions are causing automation adoption at scale. Respondents cited increasing product demand (30%) and global supply chain disruptions (26%) as the largest factors in adopting automation at scale. Tightness in access to skilled labor (13%) and reshoring of production back to North America (11%) were considered less impactful.

The robots are coming, says Vecna

“Given this data, we can see that automation has quickly become a critical strategic priority, and from the boardroom to the warehouse, leaders are looking to get robots and other warehouse technologies on the floor as soon as possible,” said Vecna Robotics.

The company said it expects the following trends this year, based on the survey data:

- High-speed, secure Internet is the biggest technology obstacle for automation adoption, so 5G wireless technology will be a high priority for companies. Updating and upgrading disparate WMS and ERP systems throughout supply chains and standardized across modern, cloud-based systems will also help alleviate some of the integration challenges currently faced by the industry.

- Consumer goods, automotive, and 3PL will continue to lead the charge in automation adoption, with retail lagging behind.

- Due to the lack of labor in pallet-moving roles, automation will be increasingly sought after to augment the talent shortage, with case picking representing the largest automation potential.

- The largest facilities will deploy automation faster.

For a more in-depth review and discussion about Vecna’s approach to deploying warehouse automation, the company offered its multi-part “From No-bot to Robot” webinar series and its automation experts for scheduling initial assessments.

Article topics

Email Sign Up

Related Materials Handling News

Related Companies