Although the potential impact of the strong dollar is causing uncertainty, optimism among U.S. industrial manufacturers for the domestic economy continues to rise, according to the Q1 2015 Manufacturing Barometer, released by PwC US.

The broad sense of optimism about overall economic conditions and improvements in global demand was offset by concerns about pricing and margins and the potential impact of currency on international revenues.

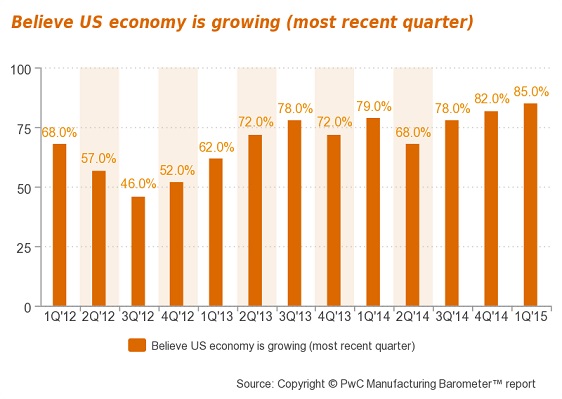

Optimism regarding the prospects of the U.S. economy during the next 12 months increased among U.S. industrial manufacturers to 76% during the first quarter of 2015, up from 68% in the previous quarter and 71% in the first quarter of 2014. The level of optimism reported was the highest since the fourth quarter of 2005. Optimism about the world economy also improved, but by a more modest four points to 42%, as compared to the previous quarter.

“A majority of management teams continue to indicate plans to hire skilled workers and invest in their businesses, with the bulk of spending centered on new products or service introductions,” said Bobby Bono, PwC’s U.S. industrial manufacturing leader. “We also saw a spike in sentiment regarding potential merger and acquisition activity, while plans to expand abroad softened, reflecting increased concerns about the impact of the strengthening dollar. Overall, the outlook for U.S. industrial manufacturers remains positive and we are seeing healthy levels of capital investment.”

Only 19% of U.S. industrial manufacturers plan to expand to new markets abroad, while only 12% plan for new facilities abroad, both down from last quarter’s barometer. Along similar lines, among respondents with international operations, the projected contribution from international sales to total revenue over the next 12 months decreased to 27%, the lowest level since the fourth quarter of 2006.

According to the survey, plans for operational spending rose to 83% of respondents, the highest level in 10 quarters. Leading increased expenditures were new product or service introductions (55%), followed by research and development (40%) and information technology (33%). In addition, plans for M&A increased during the first quarter, with 43% of respondents indicating an interest, particularly plans to purchase another business or sell part or all of their own company.

PwC’s survey also included a section on robotics systems which found that 79% of manufacturers are presently using such systems and 58% are planning to acquire more robotics systems in the next two to three years. Manufacturers are implementing robotics for a wide array of important applications led by assembly (64%), consistent high speed work (59%) and materials handling/packaging (51%), followed by visual sensors linked to computers (49%). While 49% of respondents indicated that robotics improve productivity, 69% noted that price and return on investment would have to be notably reduced before they can consider more installations.

Looking at perceived headwinds, survey respondents continued to identify lack of qualified workers (35%), legislative or regulatory pressures (33%) and lack of demand (29%) as leading barriers to growth.

Article topics

Email Sign Up

Latest Robotics News