DigiKey's European Editor via Wikimedia Commons

A new report from Interact Analysis suggests that the U.S. machine vision marketplace has several factors that will determine whether market consolidation will occur.

Get news, papers, media and research delivered. Sign up for our free newsletters.

Stay up-to-date with news and resources you need to do your job. Research industry trends, compare companies and get weekly market intelligence with Robotics 24/7.

DigiKey's European Editor via Wikimedia Commons

A new report from Interact Analysis suggests that the U.S. machine vision marketplace has several factors that will determine whether market consolidation will occur.

A new report from market research firm Interact Analysis said that U.S. machine vision market appears to be highly concentrated, but the tail of smaller vendors is vast.

The report, titled “U.S. Machine vision market: will it ever see consolidation?” outlines the various factors affecting this marketplace, and the major vendor players that accumulate most of the revenue.

Interact Analysis said that with the top three vendors making up nearly half of total revenues, it’s easy to assume the market is highly consolidated. Yet, at the other end of the market, the firm saw a highly fragmented mix of vendors accounting for much smaller slices of the market.

To answer the question related to market consolidation, Interact Analysis explored two key topics: first, how vendor concentration varies by sector, and second, what mix of sectors makes up the machine vision market.

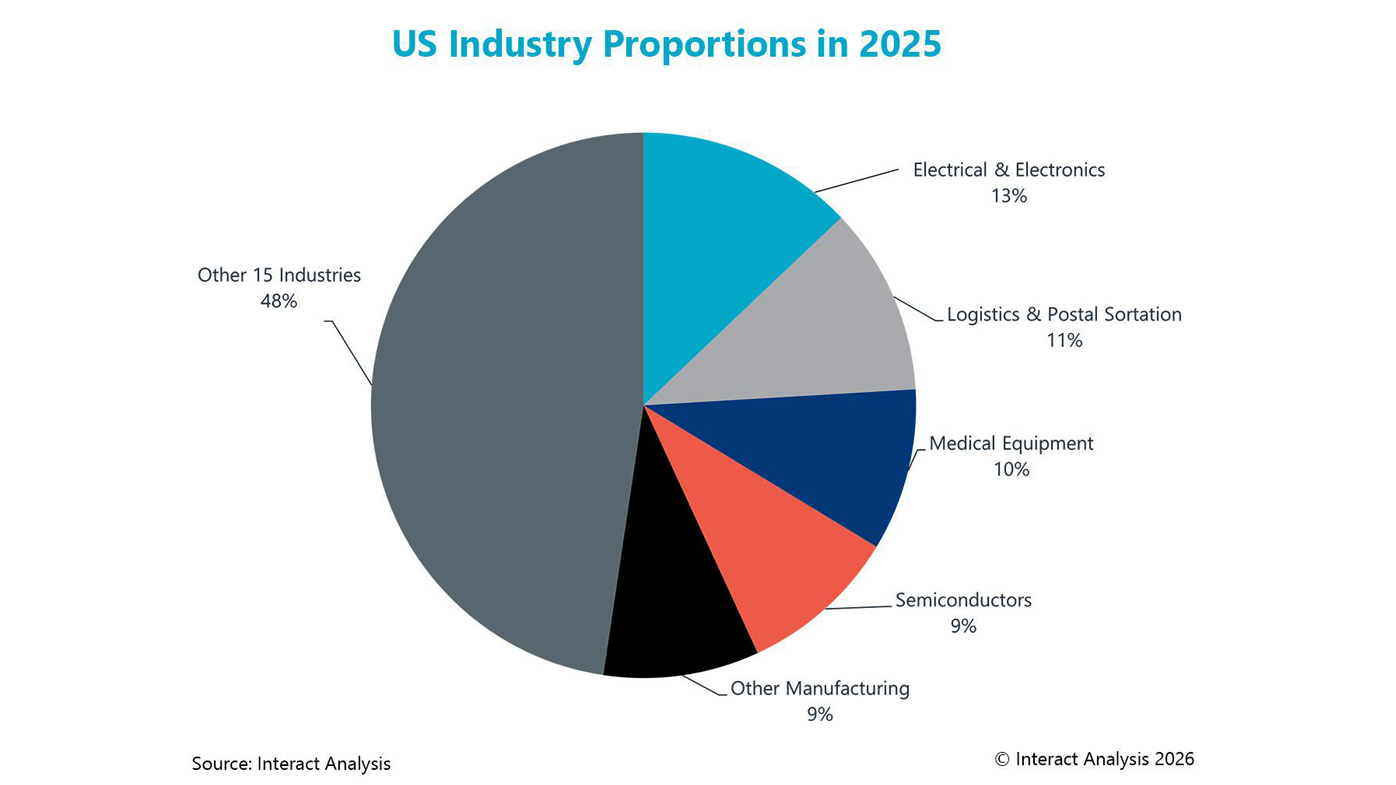

Interact Analysis said that the U.S. machine vision market, valued at $980M in 2025, is characterized by a small number of dominant vendors alongside a very long tail of smaller suppliers. Accounting for approximately 45% of the market, the research found that the top three vendors dominate, which is typical of a highly concentrated market. These three vendors focus particularly on logistics and automotive - two of the largest sectors for machine vision.

Yet, while the top three account for nearly half of the total market, IA said that there is a proliferation of smaller vendors, each focusing on specific sectors and often offering specialized equipment. The firm suggested that these sector-specific specializations create defensible moats and barriers to entry.

As a result, within each sector, Interact Analysis said that it sees strong vendor concentration. So, if each sector is concentrated, what drives the fragmented long tail of vendors at the aggregate level?

Interact Analysis said that the answer lies in the composition of sectors within the U.S. market.

The sector composition of the U.S. machine vision market consists of a few large industries and many smaller ones.

For example, of the 20 sectors covered in Interact Analysis’ research, just five account for more than 9% of the total market, while eight sectors make up less than 2%. See the wide image above for a detailed breakdown of these market segments.

IA said that this mirrors the competitive dynamic of a few large vendors and many smaller players. The firm said that vendor concentration, therefore, maps to sector composition: the largest machine vision vendors dominate the sectors that form the bulk of the U.S market, while smaller vendors with niche specializations hold stronger positions in the smaller sectors.

To understand whether the market will become more or less concentrated, Interact Analysis said that it must consider the rate of vendor consolidation as well as the evolution of sector composition.

If vendor concentration within each sector remains constant, the firm said that disproportionately high growth in smaller, niche sectors would result in a more fragmented vendor landscape. Conversely, if the large sectors that generate most revenues grow faster than the smaller, niche applications, the vendor landscape would become more concentrated.

Looking at the data, IA suggests that the four largest sectors (each accounting for 10% or more of the market) are forecast to grow at a combined CAGR of 11%, while the nine smallest sectors (each accounting for 2% or less) are expected to grow at a combined CAGR of just 9%.

Therefore, all else being equal, Interact Analysis said that the evolution of sector composition in the U.S. is expected to drive greater vendor concentration.

In short, the research firm said that there is likely to be further vendor concentration due to the growing dominance of the largest sectors, which are outpacing the growth of smaller niche segments. Additionally, IA said that ongoing vendor consolidation through acquisitions focused on gaining competencies for entry into markets with high technological barriers will also affect this marketplace.

Artificial Intelligence Machine Vision Industrial Automation Collaborative Robots Robot Arm Components Sensors Cameras Lidar Software Cloud and Edge Data Management Simulation News Press Release Interact Analysis Machine Vision Market Research Reports Mergers & Acquisitions Research and Markets

GENISOM AI makes ICRA debut at conference in Vienna

World's first omni-modal evaluation including tactile sensing for…

Ultrasonic sensing enhances robotics perception

North America’s largest automation and robotics event takes place June 22-25