Get news, papers, media and research delivered. Sign up for our free newsletters.

Stay up-to-date with news and resources you need to do your job. Research industry trends, compare companies and get weekly market intelligence with Robotics 24/7.

Recent developments in robotics, artificial intelligence, and machine learning have put us on the cusp of a new automation age.

Robots and computers can not only perform a range of routine physical work activities better and more cheaply than humans.

But they are also increasingly capable of accomplishing activities that include cognitive capabilities once considered too difficult to automate successfully, such as making tacit judgments, sensing emotion, or even driving.

Automation will change the daily work activities of everyone, from miners and landscapers to commercial bankers, fashion designers, welders, and CEOs.

But how quickly will these automation technologies become a reality in the workplace?

And what will their impact be on employment and productivity in the global economy?

The McKinsey Global Institute has been conducting an ongoing research program on automation technologies and their potential effects.

A new MGI report, A future that works: Automation, employment, and productivity, highlights several key findings.

The automation of activities can enable businesses to improve performance by reducing errors and improving quality and speed, and in some cases achieving outcomes that go beyond human capabilities.

Automation also contributes to productivity, as it has done historically. At a time of lackluster productivity growth, this would give a needed boost to economic growth and prosperity. It would also help offset the impact of a declining share of the working-age population in many countries.

Based on our scenario modeling, we estimate automation could raise productivity growth globally by 0.8 to 1.4 percent annually (see slide show).

Where machines could replace humans - and where they can’t (yet)

Explore our comprehensive data set on Tableau Public

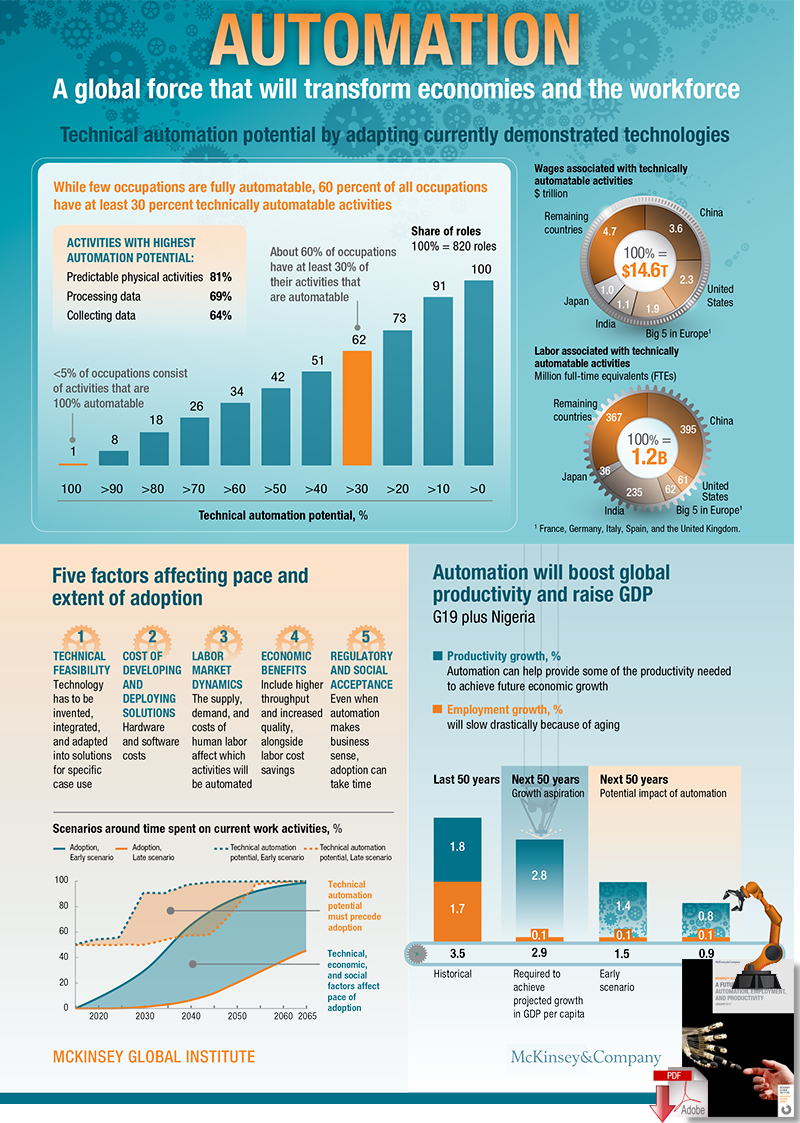

The right level of detail at which to analyze the potential impact of automation is that of individual activities rather than entire occupations. Every occupation includes multiple types of activity, each of which has different requirements for automation. Given currently demonstrated technologies, very few occupations - less than 5 percent - are candidates for full automation.

However, almost every occupation has partial automation potential, as a proportion of its activities could be automated. We estimate that about half of all the activities people are paid to do in the world’s workforce could potentially be automated by adapting currently demonstrated technologies. That amounts to almost $15 trillion in wages.

The activities most susceptible to automation are physical ones in highly structured and predictable environments, as well as data collection and processing. In the United States, these activities make up 51 percent of activities in the economy, accounting for almost $2.7 trillion in wages. They are most prevalent in manufacturing, accommodation and food service, and retail trade.

And it’s not just low-skill, low-wage work that could be automated; middle-skill and high-paying, high-skill occupations, too, have a degree of automation potential. As processes are transformed by the automation of individual activities, people will perform activities that complement the work that machines do, and vice versa.

Still, automation will not happen overnight. Even when the technical potential exists, we estimate it will take years for automation’s effect on current work activities to play out fully.

The pace of automation, and thus its impact on workers, will vary across different activities, occupations, and wage and skill levels. Factors that will determine the pace and extent of automation include the ongoing development of technological capabilities, the cost of technology, competition with labor including skills and supply and demand dynamics, performance benefits including and beyond labor cost savings, and social and regulatory acceptance.

Our scenarios suggest that half of today’s work activities could be automated by 2055, but this could happen up to 20 years earlier or later depending on various factors, in addition to other economic conditions.

The effects of automation might be slow at a macro level, within entire sectors or economies, for example, but they could be quite fast at a micro level, for individual workers whose activities are automated or for companies whose industries are disrupted by competitors using automation.

While much of the current debate about automation has focused on the potential for mass unemployment, people will need to continue working alongside machines to produce the growth in per capita GDP to which countries around the world aspire.

Thus, our productivity estimates assume that people displaced by automation will find other employment. Many workers will have to change, and we expect business processes to be transformed.

However, the scale of shifts in the labor force over many decades that automation technologies can unleash is not without precedent. It is of a similar order of magnitude to the long-term technology-enabled shifts away from agriculture in developed countries’ workforces in the 20th century. Those shifts did not result in long-term mass unemployment, because they were accompanied by the creation of new types of work.

We cannot definitively say whether things will be different this time. But our analysis shows that humans will still be needed in the workforce: the total productivity gains we estimate will only come about if people work alongside machines. That in turn will fundamentally alter the workplace, requiring a new degree of cooperation between workers and technology.

Source: McKinsey Global Institute

About the Authors

James Manyika and Jacques Bughin are directors of the McKinsey Global Institute, and Michael Chui is an MGI partner; Mehdi Miremadi is a partner in McKinsey’s Chicago office, Katy George is a senior partner in the New Jersey office, and Paul Willmott and Martin Dewhurst are senior partners in the London office.

From geometry preparation to AI-assisted analysis, integrated CFD workflows…

Software-based GripperAI manages mixed picking through basic geometry

Safety, communication and motion control components enable smooth operation

North America’s largest robotics and automation event winds down