Interact Analysis

Warehouse automation valuations spiked during the pandemic, according to Interact Analysis data.

Get news, papers, media and research delivered. Sign up for our free newsletters.

Stay up-to-date with news and resources you need to do your job. Research industry trends, compare companies and get weekly market intelligence with Robotics 24/7.

Interact Analysis

Warehouse automation valuations spiked during the pandemic, according to Interact Analysis data.

After several years of subdued deal activity, new data from market research firm Interact Analysis suggests that the warehouse automation sector appears to be entering a new phase of growth.

IA reported that because Geek+ just completed its IPO on the Hong Kong Stock Exchange, and Dexterity is preparing for a potential IPO, the market is poised for new growth.

Meanwhile, IA also said that Honeywell is reportedly exploring “strategic alternatives” for its warehouse automation business.

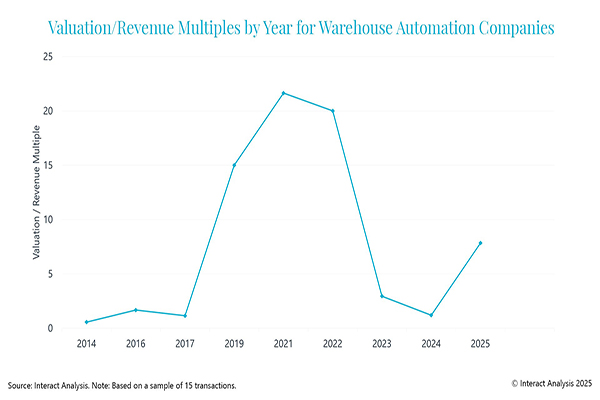

Before Covid-19, Interact Analysis reported that warehouse automation companies typically traded at revenue multiples of around 1–2x. However, demand surged during the pandemic, fueled by rapid e-commerce growth and a boom in warehouse construction.

As a result, valuations skyrocketed. Notably, AutoStore reached a 21x revenue multiple in 2022, with SoftBank acquiring a $2.2 billion stake that valued the company at $7 billion.

Similarly, Zebra Technologies acquired Fetch Robotics for $290 million (95% stake) in 2021. Based on Fetch’s “run-rate sales of approximately $10 million” at the time of the acquisition, IA said this would imply a staggering 31x revenue multiple.

However, Interact Analysis said this boom was short-lived.

As interest rates rose and e-commerce growth cooled, valuations sharply declined. By 2023 and 2024, the average valuation-to-revenue multiple had fallen to an average of 2.07x - examples such as Storage Solutions, Berkshire Grey, Alert Innovation and Siemens Logistics (Airport) all had valuation-to-revenue multiples below 5x.

But now, Interact Analysis said the data appears to suggest a rebound.

Following two years of muted activity, signs are emerging that investment in warehouse automation may be entering a new growth cycle. Interact Analysis identified the following factors that support this view:

It’s tempting to frame recent events as a simple “Covid-19 boom and bust” narrative. However, IA said the composition of companies being acquired also plays a key role in valuation trends.

System integrators focused on CapEx-heavy projects tend to receive lower valuation multiples compared with OEMs with proprietary technology and recurring revenue streams. Mobile robot vendors, particularly those offering Robotics-as-a-Service (RaaS), command even higher premiums due to their perceived stronger growth potential.

Coincidentally, IA noted that most acquisitions during the pandemic involved automation OEMs and mobile robotics providers. In contrast, pre- and post-pandemic deals have a greater composition of system integrators. This shift in deal composition partially explains the valuation spike during the pandemic, beyond just Covid-related market forces.

EBITDA multiples for conventional fixed automation system integrators hover at around 10x-20x. Storage Solutions, Intelligrated, Swisslog and Dematic were acquired at 11x, 12x, 15x and 20x EBITDA multiples, respectively. Interact Analysis said these are slightly higher than the consensus multiple for industrial machinery and equipment, which stands at 10x according to Equidam.

However, acquisitions of nascent mobile robot vendors have far higher multiples, with some vendors having negative EBITDA margins.

Geek+, for example, which listed on the Hong Kong Stock Exchange in July 2025 with a valuation of $2.8 billion, had an adjusted EBITDA of -$34 million. Many other AMR vendors that have been acquired in recent years have very low or negative EBITDA values, resulting in an extremely high EBITDA multiple.

AutoStore, which was partly acquired by Softbank in 2022 with a valuation of $7 billion, had an implied EBITDA multiple of 44x, significantly higher than its industry consensus.

In short, IA said EBITDA is often overlooked when it comes to the valuation of emerging robotics vendors, on the basis that these companies will supposedly generate significant cash flows in the future.

As such, Interact Analysis noted that investors tend to look at market potential and future growth projections to estimate future cash flows, which in turn are used to compute valuations. The issue with this approach is that the market isn’t growing as fast as it was originally touted to be.

Despite signs of renewed deal activity, the market remains volatile. Optimism at the start of 2025 faded as trade tensions and newly imposed tariffs under President Trump’s administration created economic uncertainty. This has delayed some capital investments.

Still, the outlook isn’t entirely bleak. Fixed automation orders in 2024 outperformed expectations, helping to cushion the revenue impact in 2025. Warehouse utilization is beginning to level out, particularly in the U.S., U.K. and China, where post-pandemic vacancy rates had surged. As vacancy rates start to fall from their current highs, Interact Analysis expects warehouse construction to pick up again by 2027.

GENISOM AI makes ICRA debut at conference in Vienna

World's first omni-modal evaluation including tactile sensing for…

North America’s largest robotics and automation event winds down

Automate’s largest day ever draws huge crowds to McCormick Place