Interact Analysis

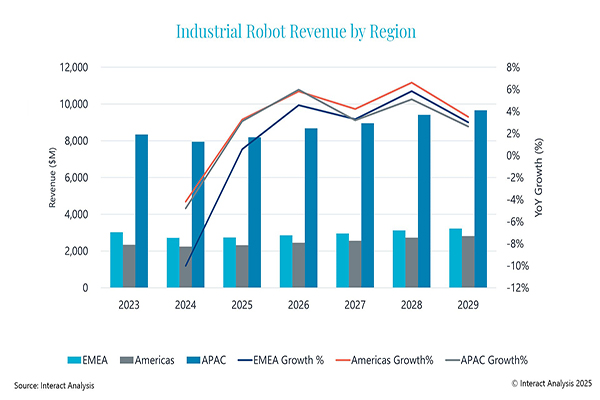

All three major regions saw robot revenue decline in 2024, with modest growth expected in 2025.

Get news, papers, media and research delivered. Sign up for our free newsletters.

Stay up-to-date with news and resources you need to do your job. Research industry trends, compare companies and get weekly market intelligence with Robotics 24/7.

Interact Analysis

All three major regions saw robot revenue decline in 2024, with modest growth expected in 2025.

The global shipment volume of industrial robots in 2024 totaled just over 505,000 units, reflecting a 2.4% decrease compared with 2023, according to a report from market intelligence firm Interact Analysis.

This reduction in shipments, coupled with a decrease in average prices, resulted in a drop in sales revenue of -5.8% year-over-year.

A slowdown in investments in the manufacturing sector has been observed across all major regions. The Asia-Pacific region saw a relatively modest decline in robot shipments at -1.1%, while the Americas and EMEA (Europe, the Middle East and Africa) experienced sharper drops of -3.7% and -8.1%, respectively.

However, while 2024 closed on a challenging note, Interact Analysis said there are signs the market will stabilize. Positive trends in some regional markets during the first quarter of 2025 support the outlook for a gradual recovery.

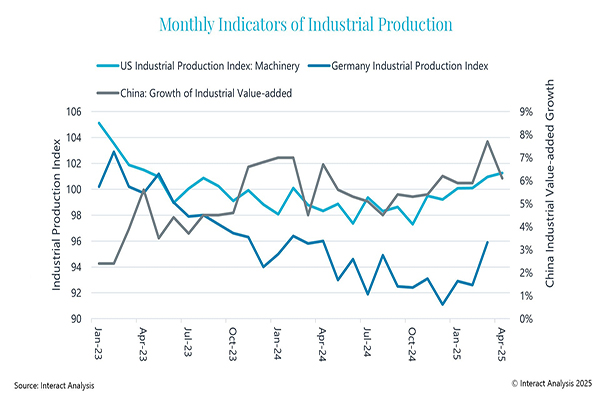

Since the second half of 2024, monthly indicators for the industrial sector in both the U.S and China have shown signs of recovery. Europe, while still trailing behind, has also begun to show improvement more recently. Although looming tariff uncertainties pose risks to machinery orders in the second half of 2025, current demand trends in major regions suggest these will not lead to a market-wide contraction.

According to the Japan Robot Association (JARA), orders for manipulators and robots rose 32.2% in Q1 2025, with export shipment value increasing by 22.8%. Interact Analysis said Japanese robot vendors, which accounted for 47% of global robot revenue in 2024, are often seen as reliable indicators of broader market health.

In this context, global shipments of industrial robots are projected to grow by 5% in 2025. However, due to continued downward pressure on average prices, revenue growth is expected to be more modest, at just 2.6%.

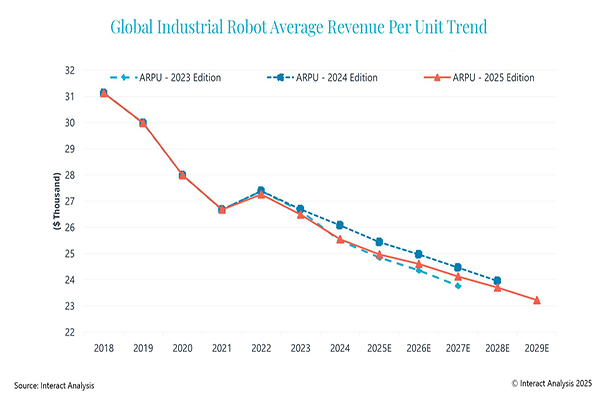

With rising production volumes and intensifying competition, the average revenue per unit (ARPU) of industrial robots declined significantly - from around $31,100 in 2018 to $25,600 in 2024. While there was a temporary price surge in 2022 amid the global supply chain crisis, prices resumed their downward trend in 2023 as demand cooled and competition increased. In 2024, ARPU fell more sharply than in previous years, dropping by -3.6% due to easing inflation and growing competition.

Fierce price competition has taken a toll on manufacturers’ margins, particularly among non-collaborative robot (cobot) suppliers, where pricing flexibility has hit its limits. Many emerging brands have aggressively pursued market share at the expense of profitability. This has led to expectations that the pace of price erosion will slow in 2025, with ARPU declining at a more moderate rate of 1%-2% annually through to 2029.

Still, certain product segments may help support pricing. Rising shipments of large-payload collaborative robots and SCARA robots could help stabilize ARPU moving forward.

Cobots have experienced the steepest declines in ARPU, largely due to the rise of low-cost, pure-play vendors. In 2023 and 2024, cobot ARPU declined by -6.4% and -4.1%, respectively, with a further -3.5% drop expected in 2025. The influx of these budget-oriented players has shifted the competitive landscape and accelerated price-based competition within the segment.

The industrial robot market has consolidated over the past few years, with the “Big 4” industrial robot manufacturers - FANUC, Yaskawa, ABB and KUKA - having long maintained a dominant position. However, 2024 marked a shift toward increased market fragmentation. The top 10 vendors saw their combined market share fall from 64.6% in 2023 to 62.3% in 2024, indicating meaningful inroads are being made by smaller and emerging players, challenging the established manufacturers amid slowing demand and increasing price pressures.

Interact Analysis said several factors contributed to this fragmentation:

In summary, Interact Analysis said 2024 was a year of contraction and strategic realignment in the industrial robot industry. Slowing shipments, declining prices and intensifying competition challenged both revenue and profitability. However, regional signs of recovery, particularly in Asia and the US, and strong order books from major players like Japanese vendors point toward a likely rebound in 2025.

The industrial robot market is undergoing a critical transition. While 2024 reflected short-term headwinds, the structural trends - automation demand, labor shortages and advances in robotics technologies - remain firmly in place. The ongoing fragmentation of the supplier base and the evolution of pricing dynamics are redefining the competitive landscape, particularly in cost-sensitive segments like collaborative robots.

Looking ahead, Interact Analysis continues to view the market with cautious optimism. As investment cycles pick up and demand stabilizes across key industries, 2025 could mark the beginning of a new growth phase, albeit one characterized by tighter margins and more nuanced competition. Robot manufacturers will need to balance innovation, efficiency and market agility to thrive in this next chapter.

From geometry preparation to AI-assisted analysis, integrated CFD workflows…

GENISOM AI makes ICRA debut at conference in Vienna

North America’s largest robotics and automation event winds down

Automate’s largest day ever draws huge crowds to McCormick Place